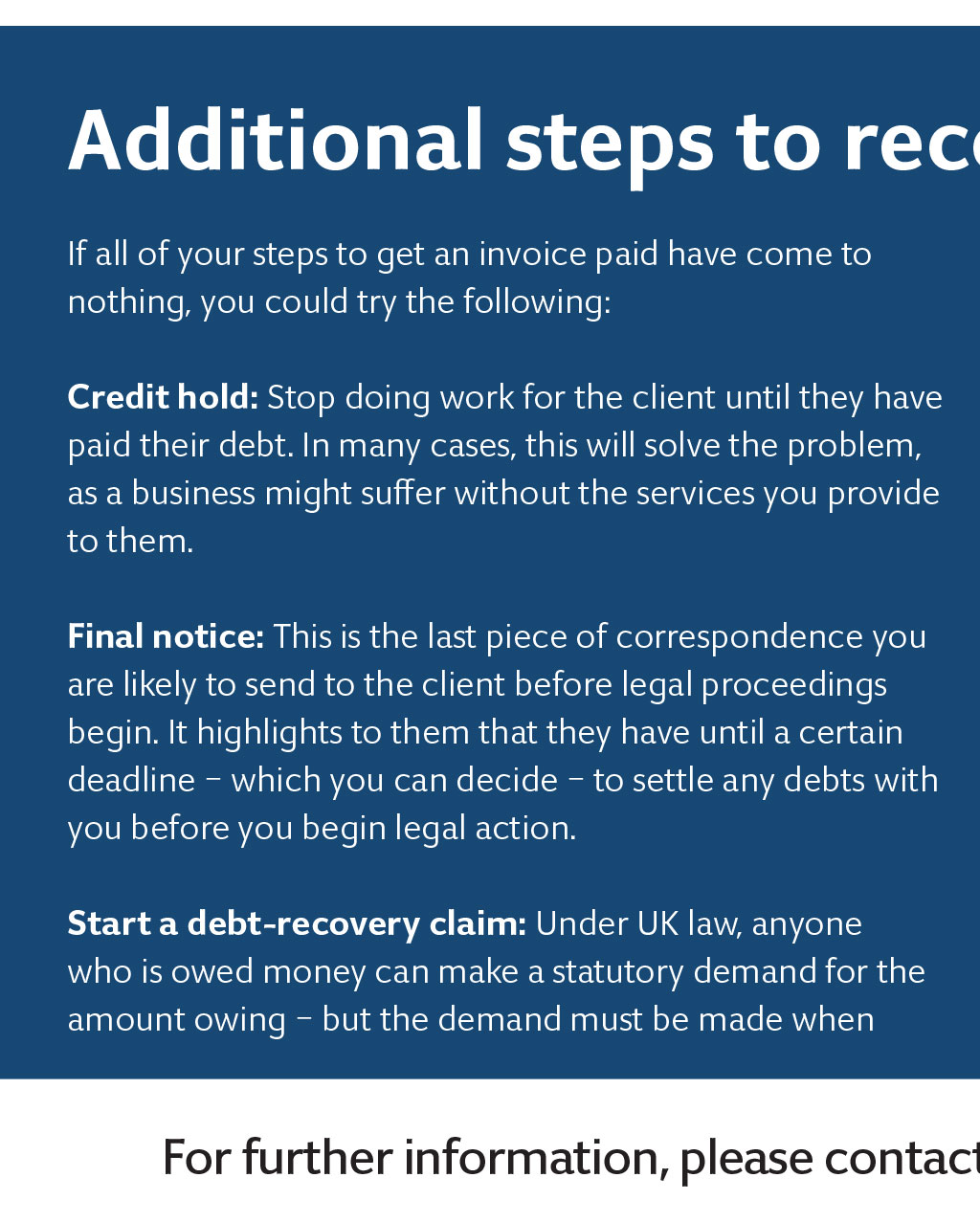

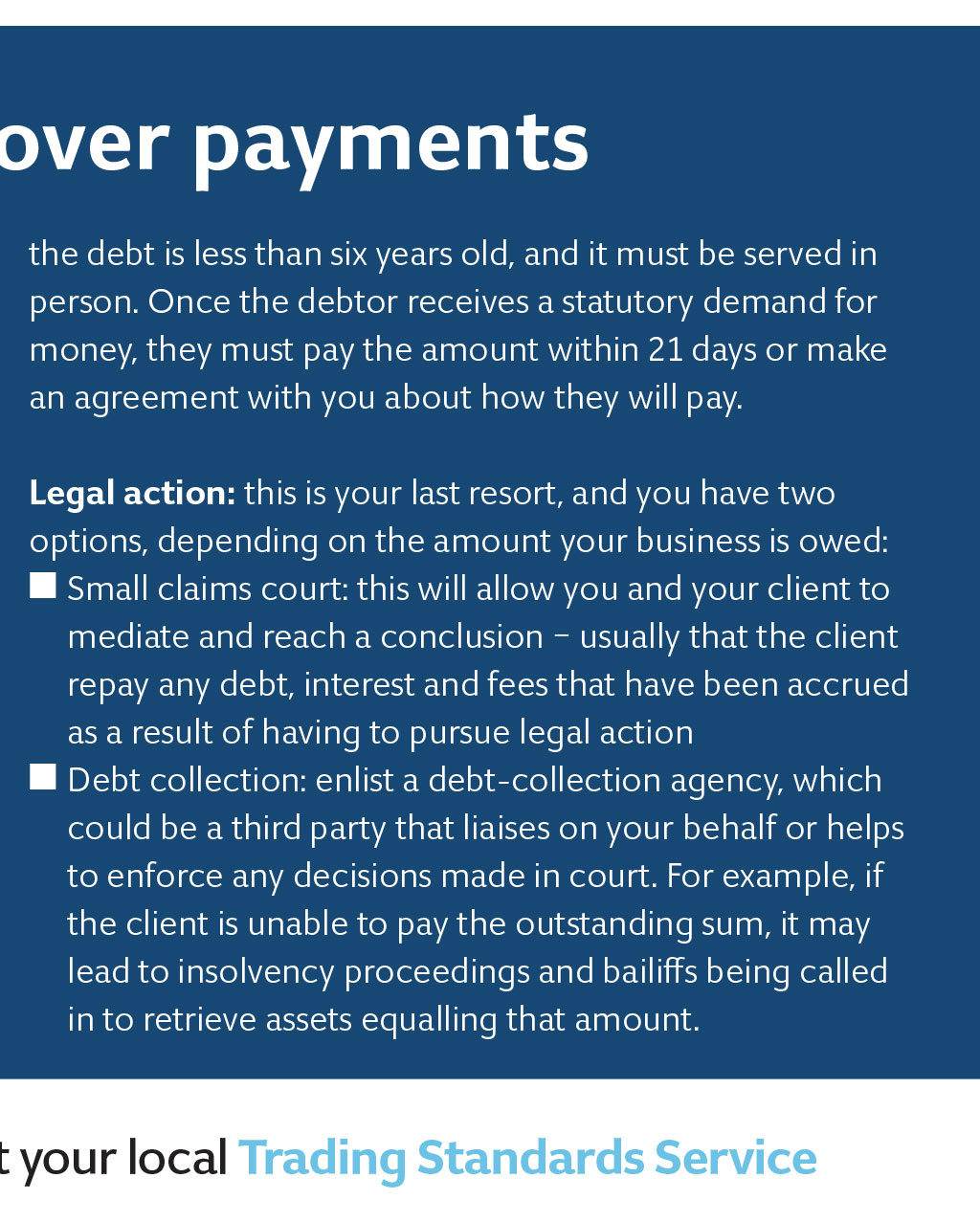

SPRING 2022 LATE PAYMENTS FINAL NOTICE DUE DEMAND DEMAND SHOW ME THE MONEY! Cash flow is vital for small businesses, so what should you do if your invoice goes unpaid? FINAL NOTICE ‘Set rules that your business will follow – and don’t go against these, even if you are put under pressure to supply goods or services urgently’ Research by the Federation of Small Businesses (FSB) shows that late payment of invoices has increased in recent months, threatening the viability of firms. Small businesses and the self-employed depend on cash flow for their very existence, so what can you do to try to prevent late payment of your invoices, or to retrieve money owed to you? Prevention is always better than cure, so before you agree to do work for a company, check its business name and legal status to establish whether credit should be offered. It can be difficult to start any legal proceedings without the correct status of a company, which may trade under a different name from the people or entity that own it. With a sole trader or partnership, the owner or partners may be personally liable, so make sure you have their full details noted down correctly. Don’t be afraid to ask for all the information you need; if you can’t get it at the start, it will certainly be harder to get it further down the line. You could also use a credit reference agency to check their details and credit status, or take references from other suppliers of the business. Set out payment terms in writing, in advance, and discuss and agree these with customers before accepting an order. Make sure the payment due date is clearly shown on invoices, and that you have a process in place for dealing with requests from customers for more time to pay. If your debt becomes overdue, call the client with a polite query; it may simply have been overlooked, but if there’s any problem, this will be an opportunity to resolve it at an early stage. Send your customer another invoice and remind them of the amount owed and the payment terms to which they agreed. Set rules that your business will follow – and don’t go against these, even if you are put under pressure to supply goods or services urgently. Whenever you write about payment terms – and on your invoices – include the words: ‘We will exercise our statutory right to claim interest (at 8% over the Bank of England base rate) and compensation for debt-recovery costs under the late-payment legislation if we are not paid according to our agreed credit terms. You are legally allowed to charge statutory interest on top of the original invoiced amount after 30 days have passed. However, if you have already listed a different interest rate in an existing contract you will not be able to charge the statutory interest rate instead. You are also permitted to charge the customer a set sum for the cost of recovering late payment, but this is dependent on the value of the debt, and you can only charge this once. If the debt still isn’t paid, send a ‘letter before action’. This requests payment within a set time period and warns of a court claim if the money isn’t paid. It is a legal requirement to send this letter if you later wish to progress proceedings. The Small Business Commissioner considers complaints from firms with fewer than 50 employees that are encountering late-payment issues with larger business customers, and offers general advice. You can also get more information from the FSB. Credit: Karen Woolley, development manager, Federation of Small Businesses Image: iStock / MicroStockHub Additional steps to recover payments If all of your steps to get an invoice paid have come to nothing, you could try the following: Credit hold: Stop doing work for the client until they have paid their debt. In many cases, this will solve the problem, as a business might suffer without the services you provide to them. Final notice: This is the last piece of correspondence you are likely to send to the client before legal proceedings begin. It highlights to them that they have until a certain deadline – which you can decide – to settle any debts with you before you begin legal action. Start a debt-recovery claim: Under UK law, anyone who is owed money can make a statutory demand for the amount owing – but the demand must be made when the debt is less than six years old, and it must be served in person. Once the debtor receives a statutory demand for money, they must pay the amount within 21 days or make an agreement with you about how they will pay. Legal action: this is your last resort, and you have two options, depending on the amount your business is owed: n Small claims court: this will allow you and your client to mediate and reach a conclusion – usually that the client repay any debt, interest and fees that have been accrued as a result of having to pursue legal action n Debt collection: enlist a debt-collection agency, which could be a third party that liaises on your behalf or helps to enforce any decisions made in court. For example, if the client is unable to pay the outstanding sum, it may lead to insolvency proceedings and bailiffs being called in to retrieve assets equalling that amount. For further information, please contact your local Trading Standards Service